Selling Property Abroad and Bringing Money Back to the UK: A Complete Guide

Table of Contents

Selling a property abroad can leave you with a large sum of money in a foreign currency. Whether you have sold a villa in Spain, an apartment in Dubai, a holiday home in France, or an investment property in Portugal, one of the most important steps is bringing the money back to the UK efficiently. For many sellers, the sale proceeds are received in euros, US dollars, UAE dirhams, Swiss francs, or another foreign currency.

If you want to bring the money back to the UK, you will usually need to convert those funds into pounds. This is where the exchange rate becomes extremely important. On a high-value property sale, even a small difference in the exchange rate can change how much you receive in sterling. If you are transferring £100,000, £250,000, £500,000 or more, the rate you achieve can make a meaningful difference.

At Overseas Payments, we help private clients move large sums internationally, convert foreign currency into pounds, and manage the currency side of overseas property sales with support from a specialist.

1. Understanding the Process

When you sell a property abroad, the money is usually paid through the local sale process. Depending on the country, this could involve a solicitor, notary, escrow account, estate agent, developer, or local bank account. Once the sale completes, you may need to transfer the proceeds back to the UK. This can involve several steps:

Confirming the final sale proceeds

Receiving the funds overseas

Checking any local deductions, taxes, mortgage repayments or legal fees

Converting the money into pounds

Sending the funds to your UK bank account

Keeping records for your accountant, solicitor or tax adviser

The process can be straightforward, but it should be planned carefully. Large international transfers often require correct documentation, compliance checks, accurate bank details and clear payment references. If you leave the currency exchange until the last minute, you may end up accepting a poor exchange rate or facing delays when trying to move the money back to the UK

2. Confirming the Currency You Will Receive

Before arranging the transfer, you need to know which currency you will receive after the overseas property sale. For example, If you sell property in Spain, France, Portugal or Italy, you may receive euros.

Once you know the currency and the expected amount, you can start planning how and when to exchange the money into pounds. This is important because exchange rates can move between the date you agree the sale and the date you actually receive the funds. For large property sale proceeds, this movement can make a significant difference to the final sterling amount.

3. Why Exchange Rates Matter on Property Sale Proceeds

When bringing money back to the UK after selling property abroad, the exchange rate determines how many pounds you receive. For example, if you sell a property in Spain and receive €500,000, the amount you receive in sterling depends on the EUR/GBP exchange rate at the time of conversion. If the rate moves in your favour, you receive more pounds.

If the rate moves against you, you receive less. Many sellers focus on the sale price, estate agent fees, legal costs and taxes, but forget that the exchange rate can also have a major impact on the final amount received in the UK.

This is especially important if you are bringing back a large amount of money. A small difference in the exchange rate may not seem important on a small transfer, but on property sale proceeds of £250,000, £500,000 or more, it can have a substantial impact. That is why comparing exchange rates before converting your funds is essential.

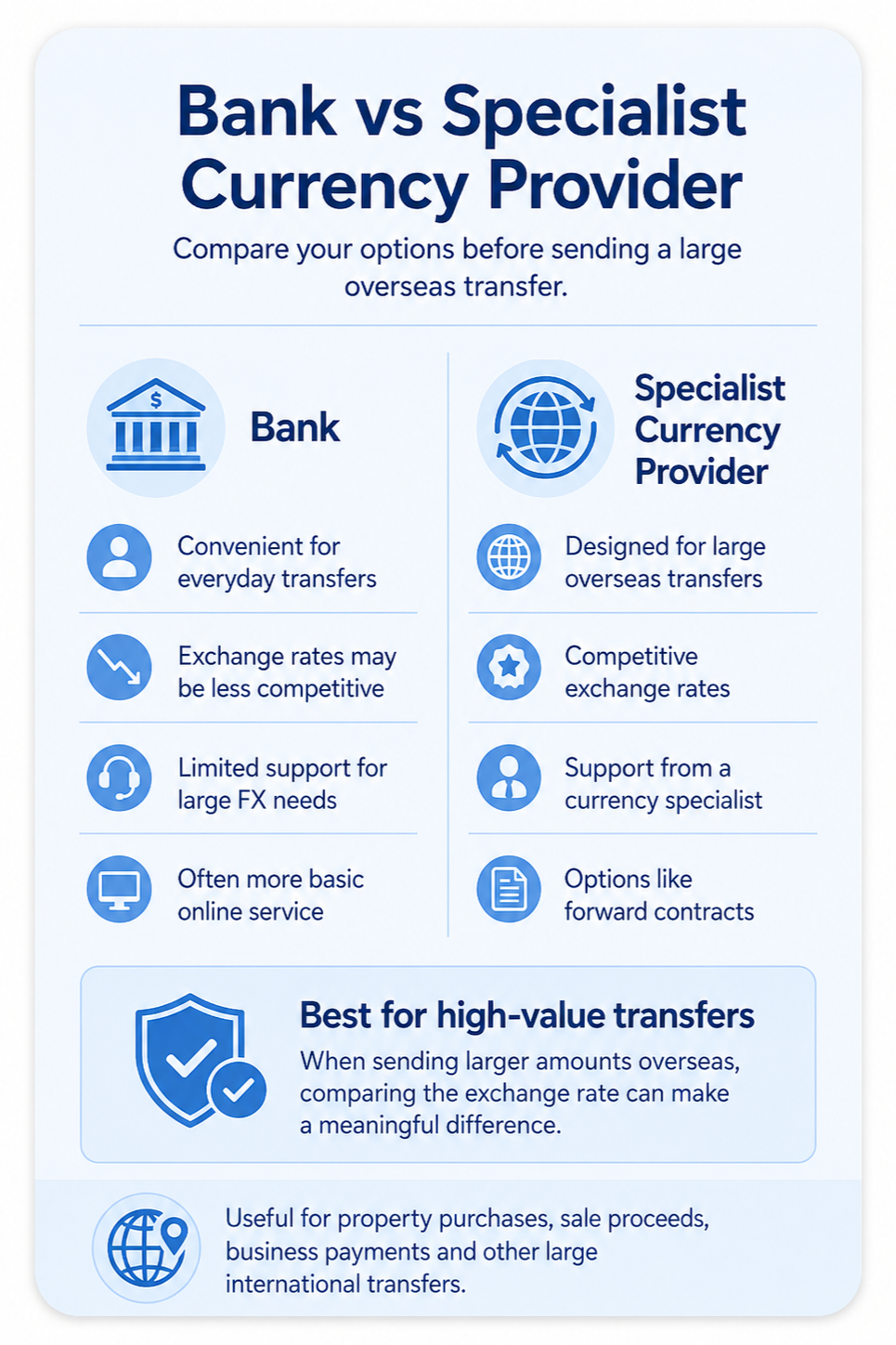

4. Bank vs Specialist Currency Provider

Many sellers first think of using their bank to bring money back to the UK. Banks are familiar and convenient, but they may not always offer the most competitive exchange rate for large international transfers. For high-value property sale proceeds, the exchange rate is usually far more important than the visible transfer fee.

A specialist currency provider may be able to help you: Compare the exchange rate against your ban Convert large sums from euros, dollars, dirhams or another currency into pounds Plan the timing of your transfer Discuss forward contracts for future property sale proceeds Understand what information may be required before sending funds

Speak to a currency specialist rather than relying only on online banking When transferring large property sale proceeds to the UK, it is worth comparing your options before converting the money. Even a small improvement in the exchange rate can make a meaningful difference.

5. Bringing Large Sums Back to the UK

Bringing a large amount of money back to the UK is not the same as making a small online transfer. If you are transferring £100,000, £250,000, £500,000 or more, the process should be handled carefully. Before arranging the transfer, you should confirm:

The exact amount being transferred

The currency being sold

The currency being bought

The UK bank account receiving the funds

The expected arrival time

Any transfer limits

Any documents required

The exchange rate being offered

The total amount you expect to receive in pounds.

It may also be worth speaking to your UK bank before receiving a large incoming payment, especially if the amount is significant.

This can help avoid confusion when the funds arrive. You should also keep records of the property sale, the transfer confirmation and the exchange rate used. These records may be useful for your accountant, solicitor or tax adviser.

6. Selling Property in Spain, France, Portugal or Dubai

Different countries have different sale processes, but the currency issue is often similar. You are selling an overseas asset and need to convert the proceeds back into pounds.

Selling Property in Spain

Many UK residents own property in Spain. If you sell a Spanish property and receive euros, you may want to convert those euros into pounds and transfer the money to your UK bank account. Before doing this, make sure you understand the final amount available after any local costs, legal fees, mortgage repayment or tax deductions. Once you know the net amount, you can compare exchange rates and decide when to convert the money.

Selling Property in France

If you sell property in France, your proceeds may also be received in euros. The EUR/GBP exchange rate will affect how much you receive when the funds are converted into pounds. For high-value French property sales, even a small rate difference can materially affect the final sterling amount.

Selling Property in Portugal

Portugal remains popular with UK buyers, retirees and investors. If you sell a Portuguese property and need to bring funds back to the UK, planning the currency exchange early can help you avoid rushing the transfer. This is particularly important if you intend to use the sale proceeds for another property purchase, investment, or major financial commitment in the UK.

Selling Property in Dubai

Dubai property sales may involve UAE dirhams or US dollar-linked pricing. If you are bringing money back to the UK, the AED/GBP or USD/GBP conversion will affect the final amount received. High-value Dubai property sales can involve substantial sums, so comparing exchange rates before moving funds is particularly important.

7. Documents You May Need

When transferring large property sale proceeds, you may be asked to provide documents to support the source of funds.

This is normal for high-value international transfers. Documents may include:

Property sale contract

Completion statement

Notary or solicitor confirmation

Proof of property ownership

Bank statement showing receipt of sale proceeds

Identification documents

Proof of address

Tax or legal documents connected to the sale

The exact documents required will depend on your circumstances, the country involved and the payment provider.

Having these documents ready can help avoid delays. If you are unsure about tax, legal or reporting obligations, you should speak to a qualified tax adviser, accountant or solicitor. Overseas Payments can help with the foreign exchange and international payment side, but we do not provide tax or legal advice.

8. Protecting Your Exchange Rate Before Completion

If your property sale has not yet completed, you may still be exposed to exchange rate movements. For example, you may agree to sell a property in Spain for €600,000, but completion may not happen for several weeks or months. During that time, the EUR/GBP exchange rate can move. This means the sterling value of your sale proceeds can change before you receive the money.

A forward contract may allow you to lock in an exchange rate for a future transfer. This can help you know in advance how many pounds you will receive when the overseas property sale completes.

Forward contracts can be useful if:

You have agreed a sale price but completion is in the future

You want certainty over the sterling value of your sale proceeds

You are worried the exchange rate could move against you

You need to plan a UK property purchase or investment after the sale

You have a fixed sterling target in mind

A forward contract protects you if the exchange rate moves against you. However, if the exchange rate moves in your favour, you will not benefit from the improved rate. Forward contracts are designed for certainty, not speculation.

9. Common Mistakes to Avoid

When selling property abroad and bringing money back to the UK, avoid these common mistakes.

Waiting Until Completion to Think About Currency

Many sellers only think about currency exchange after the sale completes. By then, the exchange rate may have moved significantly. If the transfer amount is large, this can have a major impact on the final sterling amount.

Only Looking at Transfer Fees

A low transfer fee does not always mean you are getting the best deal. On large transfers, the exchange rate is usually the biggest cost.

Using the First Rate Offered

Before converting large property sale proceeds, compare your bank’s rate against a specialist currency provider.

Not Preparing Documents

Large transfers can require source-of-funds checks. If you do not have the right documents ready, your payment may be delayed.

Sending Funds Without Checking Bank Details

Incorrect bank details can delay or return the payment. Always verify the receiving account before transferring funds.

Ignoring Tax or Legal Advice

Selling property abroad may have tax or legal implications. Speak to a qualified adviser before making decisions.

Forgetting About Exchange Rate Risk

If completion is weeks or months away, the exchange rate can move before you receive your proceeds. A forward contract may help protect the sterling value.

10. How Overseas Payments Can Help

Overseas Payments helps individuals and businesses move money internationally. If you are selling property abroad and bringing money back to the UK, we can help with the currency exchange and international payment side of the process. We can assist with:

Converting euros into pounds

Converting US dollars into pounds

Converting UAE dirhams into pounds

Large international transfers to the UK

Repatriating property sale proceeds

Comparing exchange rates

Forward contracts for future sale proceeds

Support from a currency specialist

Our service is designed for clients who are moving meaningful sums and want support throughout the process. Whether you are selling property in Spain, France, Portugal, Dubai, Italy, the USA or another country, we can help you understand your options before converting your funds. We do not provide tax, legal or investment advice, but we can help you manage the foreign exchange and international payment process.

11. Conclusion

Selling property abroad can create a major currency decision. Once your sale proceeds are available, the exchange rate you receive will determine how much you bring back to the UK in pounds. For high-value property sales, even a small difference in the exchange rate can make a meaningful difference to the final amount received. The best approach is to plan early, compare exchange rates, prepare your documents and avoid leaving the currency exchange until the last minute.

At Overseas Payments, we help clients bring large sums back to the UK after selling property overseas. If you have sold, or are planning to sell, a property abroad, speak to Overseas Payments before converting your funds.

Thank You!

We've received your enquiry. A member of our team will be in touch shortly.